Nonetheless, fund managers are tasked with interpreting data and predicting future trends to allocate clients’ capital efficiently. With the 2017 ‘Investing in African Mining Indaba’ how should they be thinking?

Investment in mineral and metals exploration in Africa has been declining sharply (especially in South Africa), despite a forecast recovery for some commodity prices. Beyond the immediate question of where commodity prices are headed over the next few years, a longer-term question also needs to be answered – how might different commodity prices move against the broader backdrop of Trump’s brave new world, and the impending Fourth Industrial Revolution – quantum technological advances that will change the world as we know it? What implications do changing geopolitics and disruptive new technologies have for African countries’ growth prospects? How should African policymakers position their countries to take advantage of natural endowments and offer value to investors?

The latest World Bank Commodity Markets Outlook is an instructive place to begin. It forecasts the price of crude oil to climb from an average of $43/bbl in 2016 to $60/bbl in 2018. That is mixed news for African countries. For Nigeria and Angola, it makes the distribution of patronage difficult and portends a likely continued budget deficit. But political stability (tenuous in Angola) is more likely than had the price plateaued at its 2016 average. Either way, the new price generates a strong incentive for economic diversification. For countries with large recoverable oil and gas reserves (like Uganda, Tanzania and Mozambique), growth prospects are potentially more promising than this time last year, but it’s not clear that this is where these countries should focus their economic efforts:

As a recent book, Blood Oil, points out, the most oil-wealthy countries in Africa are also the worst-governed – their citizens have the worst Human Development Index scores and the lowest degrees of civil liberty. Windfall oil rents can sever citizen-state accountability links, as ruling elites no longer require tax revenue from other sources. It is also cheaper in political calculus to repress than to reform in the direction of democracy. A long-run oil price ceiling of $50/bbl may therefore be good news for ordinary African citizens, as it puts fewer rents in the hands of potentially repressive elites.

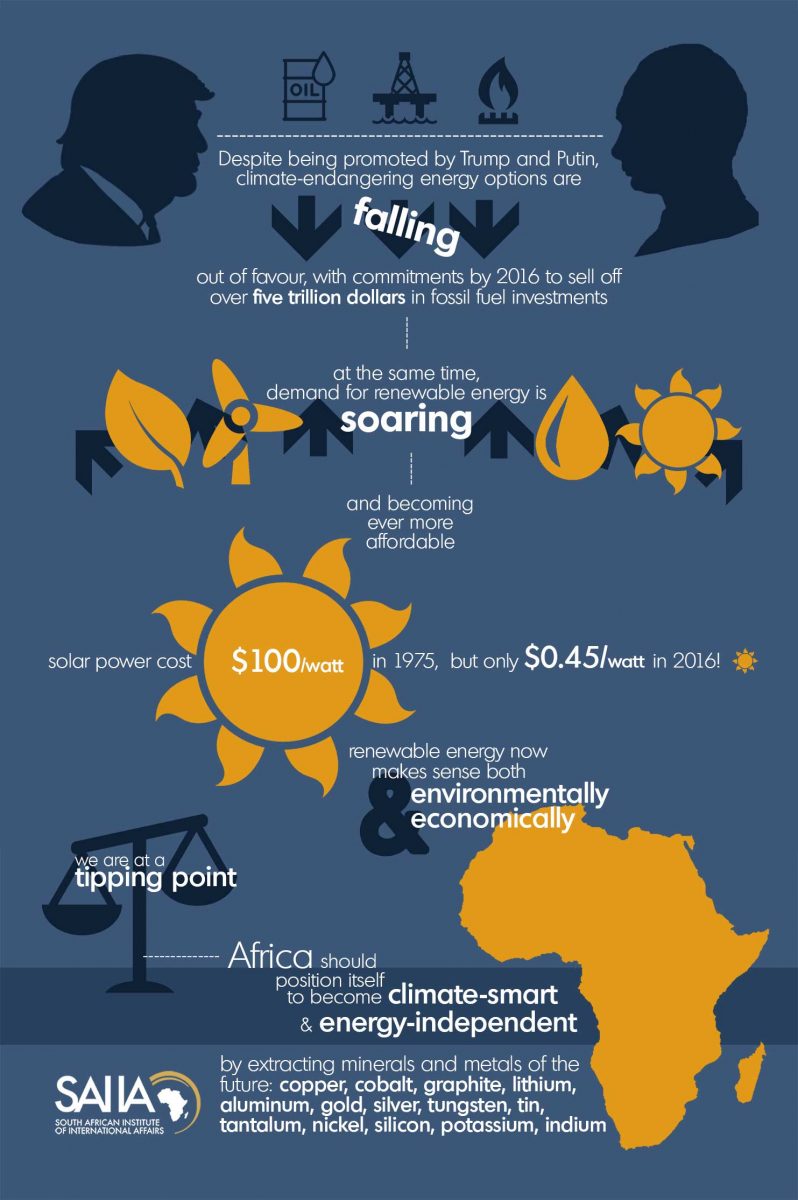

Many funds are divesting from fossil fuels already, so it would seem unwise to try and buck this trend.

Metals and minerals, on an index benchmarked at 100 for 2013, are projected to climb from 67 in 2016 to 70 in 2018. Copper prices, as one example, are up 17.4% on this time last year. Precious metals (including platinum) will decline from 97 to 90. The platinum price appears to be hovering at around $970/oz, but should pick up if fuel cell technology takes off. The gold price, which averaged $1,249/oz in 2016, is projected to decline to $1,138 in 2018. That is surprising in the face of future geopolitical turmoil, as gold has traditionally been a refuge under uncertainty. While central bank gold purchases are generally up, consumer demand for jewellery remains stubbornly low.

Coal prices are moving back towards $90/ton, but the International Monetary Fund (IMF) expects this to be a temporary phenomenon attributable to short-term supply disruptions. Prices are likely to decline sharply within a year.

On the merits of recent price movements and future potential, then, copper and platinum appear to be more attractive investments than oil and coal, while gold remains unclear.

Enter Trump, Brexit and the Fourth Industrial Revolution – major harbingers of uncertainty, which will play out against Putin’s ambitions to make Russia great again. There are three dimensions to this scene that will affect the prospects of mineral and hydrocarbon-centred African countries.

First, Trump threatens to reverse global progress on mitigating climate change. The recent Paris agreement may withstand what the US does, as each country has made its commitments relatively independently. Trump has promised to cancel the agreement within his first 100 days of office, but he can’t – he must wait three years before filing notice to withdraw. Even so, US reversal would have a negative impact on curbing the 17.89% of global emissions for which the US is responsible. Fossil fuel demand may increase in the short run, but it’s not clear that policymakers or investors should respond.

Second, Trump has promised to bring coal mines back online. But the reality of the electricity sector in the US is that coal mines only employ about 60,000 people, and coal only generates 33% of the country’s electricity, on par with natural gas. Natural gas and oil extraction, however, employ 285,000 people. Solar power, providing only 1% of the country’s total electricity so far, already employs 209,000 people. Trump will therefore find it difficult to bring redundant coal mines back online. For African countries that were hoping for new coal markets, such a move probably wouldn’t have benefited them anyway, as it would have been ‘America first’ (favouring American over Africa suppliers).

Besides, demand for coal-fired power is declining: Marginal costs of coal extraction to feed coal-fired power stations continue to rise while the levelized costs of solar and wind power continue to decline. The IMF reports that the cost of solar PV declined by 66% between 2009 and 2016. In South Africa, new wind and solar is less expensive per KWh than new coal (thanks to Medupi and Kusile cost overruns). A recent research report showed that optimally-positioned solar and wind farms could supply all South Africa’s electricity requirements with occasional supplementation from open cycle gas turbines. This kills the politically expedient argument that we require coal and nuclear to satisfy baseload demand. Investors should not be duped.

Third, Putin (and his relationship with Trump) muddy the global energy waters. Putin has allegedly boosted right-wing populists across Europe and elsewhere in the world, using energy deals as his preferred vehicle of cash transfer. Trumping up political support for gas pipeline and nuclear reactor projects may increase gas and uranium demand, leading some investors to expect price hikes. South Africa knows this story only too well. Gupta business interests bought Shiva uranium mine at a steal, for instance, allegedly with insider information about a fait accompli nuclear deal. But most investors would do well to stay away from nuclear and uranium.

Thankfully, the economic arguments in favour of supporting a fossil-fuel and/or nuclear-dominated global electricity sector are weak. Subsidies for renewable energy development were long-viewed as inefficient. But the tipping point for wide-scale switching to wind and solar is near. There are political barriers, as Eskom has shown in delaying the next Independent Power Producer bidding window, but these will ultimately be overcome as wasteful state-owned enterprises go bust.

Sustaining arguments against fossil fuel and nuclear investment, the Fourth Industrial Revolution is here. That means at least two important things for how African policymakers and global investors should be thinking.

First, the demand for wind and solar power will continue to soar. Big data, 3D manufacturing, the Internet of Things, and self-driving cars, all require smart, decentralised energy provision. Solar panels require at least 16 different minerals, metals or rare earth elements. Wind turbines require at least 13.

Second, smartphone penetration will continue to proliferate, especially into the most remote parts of Africa. Aside from the potential market benefits of newly connected people, the minerals and metals required for smartphone production are also extensive. In other words, despite recycling efforts, the demand for many minerals and metals is not going away.

Policymakers across Africa should therefore make every effort to align minerals and industrial policies to take advantage of these dynamics. Exploration should be incentivised and investments made in building sound geological knowledge. National development plans should treat the extractive industries as a lever for sustainable growth.

Many African countries are at risk of what Dani Rodrik calls ‘premature de-industrialisation’. The advance of new technology provides an opportunity to tap into new value chains and avert this. This means using one’s natural resource endowment in a way that doesn’t perpetuate over-dependence on raw material exports. It may mean abandoning projects like coal mining – that entail extensive hidden environmental and health costs – in favour of copper and platinum projects, for instance.

Improved terms of trade are possible. But African countries will require more mature leadership to eschew third-termism and overcome a Trumputin global order that threatens to shunt us back to a fossil-fuel-intensive dark age. Africa should position itself as climate-smart and energy-independent. Our future depends on it, because the Fourth Industrial Revolution will leave Africa even further behind if its disruptive effects are not anticipated and turned into future economic advantage.